NVIDIA’s $4B CPO Bet: Scale‑Out First, Scale‑Up Later — The Adoption Curve Investors Should Underwrite

On March 2, 2026, NVIDIA announced a $4B investment split between Coherent and Lumentum. The headline number is actually two coordinated moves — $2B into Coherent and $2B into Lumentum — each tied to multi‑year purchase commitments and capacity/priority access aimed at scaling co‑packaged optics (CPO).

Coherent makes the linkage explicit in its own 8‑K, disclosing that the collaboration expands NVIDIA’s access to “five additional product families related to co‑packaged optics,” while NVIDIA has already telegraphed CPO networking as a path to scaling “AI factories” via Quantum‑X Photonics and Spectrum‑X Photonics.

In real CPO deployments, lasers are often pushed out of the hot ASIC package into external laser source modules that are thermally isolated and field‑replaceable, feeding silicon photonics engines near the switch. The Lumentum leg completes the picture: it looks like NVIDIA underwriting the laser bottleneck that CPO architectures expose.

Lumentum had already begun expanding U.S. manufacturing for CPO‑relevant laser capacity, and NVIDIA’s investment reads less like a sudden pivot than a deliberate sequence: supplier builds the capacity roadmap → NVIDIA finances and reserves it as CPO ramps.

The investor takeaway is blunt: this is not just demand pull, it’s supply gating; CPO shifts what must be secured upstream (lasers, advanced optics, integration capacity rather than just pluggable modules); and the fact that the deals are nonexclusive signals a multi‑sourcing strategy, not vertical capture.

Secondly, let’s look at the data outlined in the McKinsey projections. It illustrates exactly why hyperscalers are being forced to rethink their architectures.

Source: McKinsey Report on Networking Optics

By 2029, total transceiver demand is projected to double to 28 million units, with a staggering 41% concentrated strictly in the 1.6 Tbps segment. While highly engineered OSFP pluggables can technically survive at these 1.6T speeds, they will not thrive.

Pushing legacy form factors to 1.6T exacts a massive power penalty—often requiring 30 to 40 watts per module—which pushes conventional air cooling to its absolute physical limits. If the industry attempts to meet this 11-million-unit demand exclusively with these power-hungry pluggables, data centers will rapidly exhaust their facility power budgets. Therefore, this chart does not just map the growth of the transceiver market; it pinpoints the exact capacity threshold where the massive power tax of 1.6T pluggables forces CPO out of R&D and into mandatory deployment.

We do not have to guess CPO timeline. The public markets are already flashing concrete leading indicators for CPO deployment:

NVIDIA CPO switching systems commercialization: NVIDIA’s technical blog states customers and commercial availability targets of early 2026 for Quantum-X InfiniBand photonics switches and 2H 2026 for Spectrum-X Ethernet photonics switches

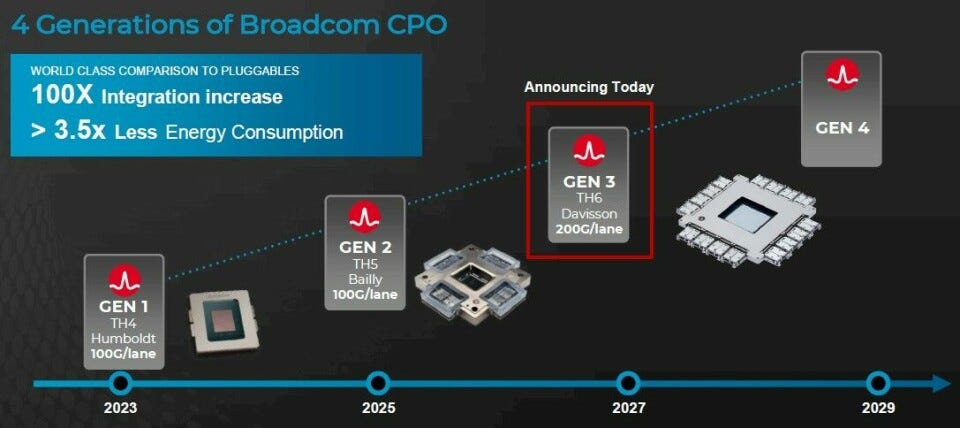

Broadcom CPO shipping (hyperscaler early deployments): The Next Platform reports Broadcom’s second-generation CPO (“Bailly”) Gen 1 began shipping to hyperscaler customers in 2023 and provides concrete per-port power comparisons versus pluggables.

Hyperscaler bandwidth mix shift (demand pull): McKinsey projects hyperscalers will shift ~87% of back-end optics to 800G and above by 2029, with 1.6T transceivers >40% of that back-end demand.

Supply pressure (forcing function): McKinsey also projects 800G transceiver production could fall 40–60% short of demand through 2027, and 1.6T supply shortfalls of 30–40% through 2029—which tends to accelerate architectural substitutions (LPO, on-board optics, CPO) where feasible.

Our clients are also wondering about Applied Optoelectronics and record braking performance. We will also comment on AAOI’s Moat.

In today’s article, we’ll address client asked questions that determine whether CPO becomes a lasting structural shift. Note: This piece focuses on recent market catalysts rather than foundational engineering. For a breakdown of the technical contrasts between CPO and traditional pluggables, please refer to our 2024 architectural deep dive.

If pluggables (OSFP/QSFP-DD) can scale to 1.6T, What is the bull case for Co-Packaged Optics (CPO)?

Applied Optoelectronics’s pluggable Moat:

Is AAOI’s 400mW pump laser a credible pivot—or too small?

Why would a hyperscaler choose AAOI for transceivers over Coherent/Lumentum/Broadcom?

Discuss key CPO adoption concerns and give our take

Adoption pace (scale-up vs. scale-out):

How quickly will co-packaged optics (CPO) be adopted in scale-out data center fabrics versus scale-up accelerator interconnects, and what specific workloads, network tiers, or deployment environments will drive the earliest production use?Value chain and value capture:

As the industry shifts from front-panel pluggable optics to CPO/near-ASIC optical engines, how does the content and profit pool redistribute across the value chain?

What are the second-order effects of CPO on today’s optical and networking supply chain—who gets disintermediated, which components become bottlenecks, and what does this mean for incumbents in transceivers, components, and manufacturing services?

Upstream equipment suppliers that benefit:

Which upstream equipment and “picks-and-shovels” suppliers are likely to see outsized demand from CPO adoption and why?

Please note: The insights presented in this article are derived from confidential consultations our team has conducted with clients across private equity, hedge funds, startups, and investment banks, facilitated through specialized expert networks. Due to our agreements with these networks, we cannot reveal specific names from these discussions. Therefore, we offer a summarized version of these insights, ensuring valuable content while upholding our confidentiality commitments.

Q1. Pluggables vs. bull case for CPO & Our Take on Concerns

At first glance, the existence of 1.6T pluggables raises a fair question: if the interface already scales, why introduce architectural complexity with co‑packaged optics? The answer lies not in whether pluggables work, but in whether they remain the most efficient system-level solution as bandwidth, density, and AI-driven scale accelerate. To evaluate the bull case for CPO, we need to look beyond module capability and examine system constraints.

We need to look at OSFP not as a permanent cure, but as the ultimate, highly engineered band-aid.

OSFP is brilliant, and it is the exact reason data centers can survive 800G and early 1.6T speeds right now. By making the pluggable module slightly larger and strapping a massive heat sink to it, OSFP buys the industry time.

When you see Applied Optoelectronics’ stock rally, it can be confusing at first. If NVIDIA and others are pushing hard toward co-packaged optics, why is a pluggable transceiver supplier like AAOI gaining traction?

The key distinction is:

“Can a pluggable module exist at 1.6T?” → yes.

“Is a pluggable architecture still the best system architecture at 1.6T+ AI scale?” → often not.

We don’t need CPO because pluggables “can’t do 1.6T.” We need CPO because at 1.6T and beyond, pluggables can become too power-hungry, too thermally constrained, and too electrically lossy for the densest AI fabrics.

Applied Optoelectronics’s Moat in Pluggables

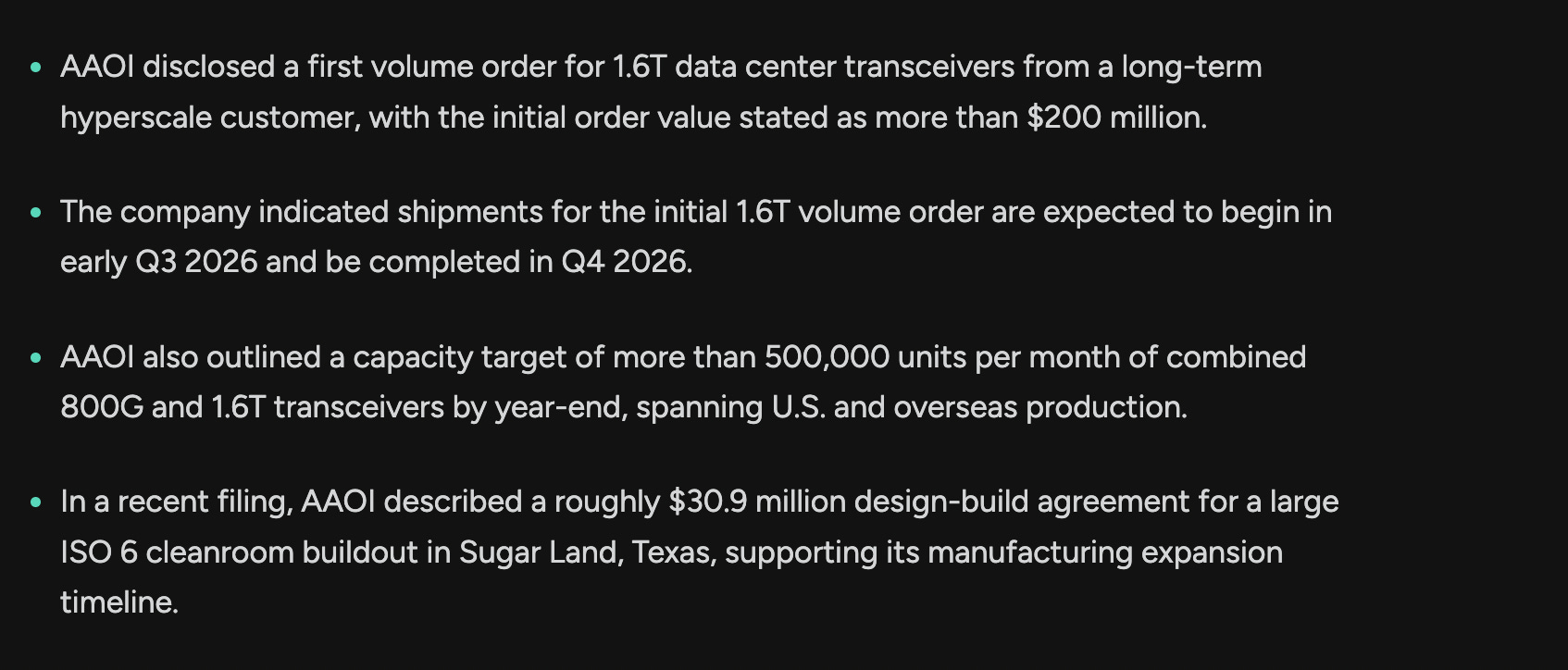

Today, On March 9th, Applied Optoelectronics announced that it received its first volume order for 1.6T data center transceivers from a major hyperscale customer possibly suspected Amazon and the stock jumped! Our clients are wondering ,Why would a hyperscaler choose AAOI for transceivers over Coherent / Lumentum / Broadcom? And if their InP manufacturing capacity is a real moat?

The customer order details say,

AAOI occupies a specific position in the data center value chain. They don’t manufacture switches, servers, racks, or cabling infrastructure; instead, they focus on the optical transceivers that move data between those systems.

AAOI’s CFO outlined a mid‑2027 monthly transceiver revenue run-rate target near $378M/month (mix: $91M 100/400G, $217M 800G, $71M 1.6T), based on three hyperscale customers. That’s the opposite of a company being “immediately disrupted” by CPO—AAOI is effectively saying the next 18–24 months are dominated by pluggable ramps.

As we discussed regarding CPO and 1.6T pluggables, the entire industry is facing a component urgency and future shortage. The ultimate chokepoint is not assembling the metal boxes; it is the fabrication capacity for Indium Phosphide (InP) laser diodes.

Unlike many module vendors that simply buy lasers from third parties and assemble them, AAOI manufactures its own lasers in-house.

Because they control the raw “fuel” (the lasers) required for both modern pluggables and future CPO external light sources, hyperscalers are flocking to AAOI to bypass the broader supply chain gridlock.