In our previous piece, “The ROI Math Behind Humanoids in Manufacturing,” we unpacked where the economics of humanoid deployment finally start to make sense—how labor substitution, uptime, and CapEx amortization align to create real financial return. That analysis triggered a flood of follow-ups from clients who wanted to go deeper—not into the mechanics or battery chemistry, but into the data economics behind the machines. Investors are now asking sharper questions: What does the robotics data chain actually look like? Who owns it? And what role do players like Scale AI, iMerit, and Encord play in that emerging ecosystem?

Those questions are landing just as production ramps at an unprecedented pace. Tesla expects to produce 500 000 humanoids by 2027, giving it more robots than Japan’s current industrial-robot base.

Figure, Agility Robotics, and BYD are right behind, each targeting between 10 000 and 200 000 units within the next two to three years—effectively creating the world’s first supply chain for human-form automation. At these volumes, even conservative adoption means millions of motion hours per week—a torrent of sensor data no single robotics firm can label or train on alone. That’s why attention—and capital—is shifting toward data-refinery companies like Scale AI, the invisible layer that transforms raw robotic motion into learning fuel.

Zooming out, Morgan Stanley projects the humanoid-robotics market could exceed $5 trillion by 2050, with more than 1 billion humanoids operating across homes, warehouses, and factories.

In the nearer term, Bain & Company’s 2025 Technology Report notes that the sector attracted roughly $2.5 billion in venture capital during 2024. The investment thesis is converging: once robots master reliable movement and dexterity, the limiting factor won’t be metal or cost—it will be data, and who controls the continuous learning loop that turns it into intelligence.

In today’s article, we’ll dig into the questions that have dominated recent client conversations:

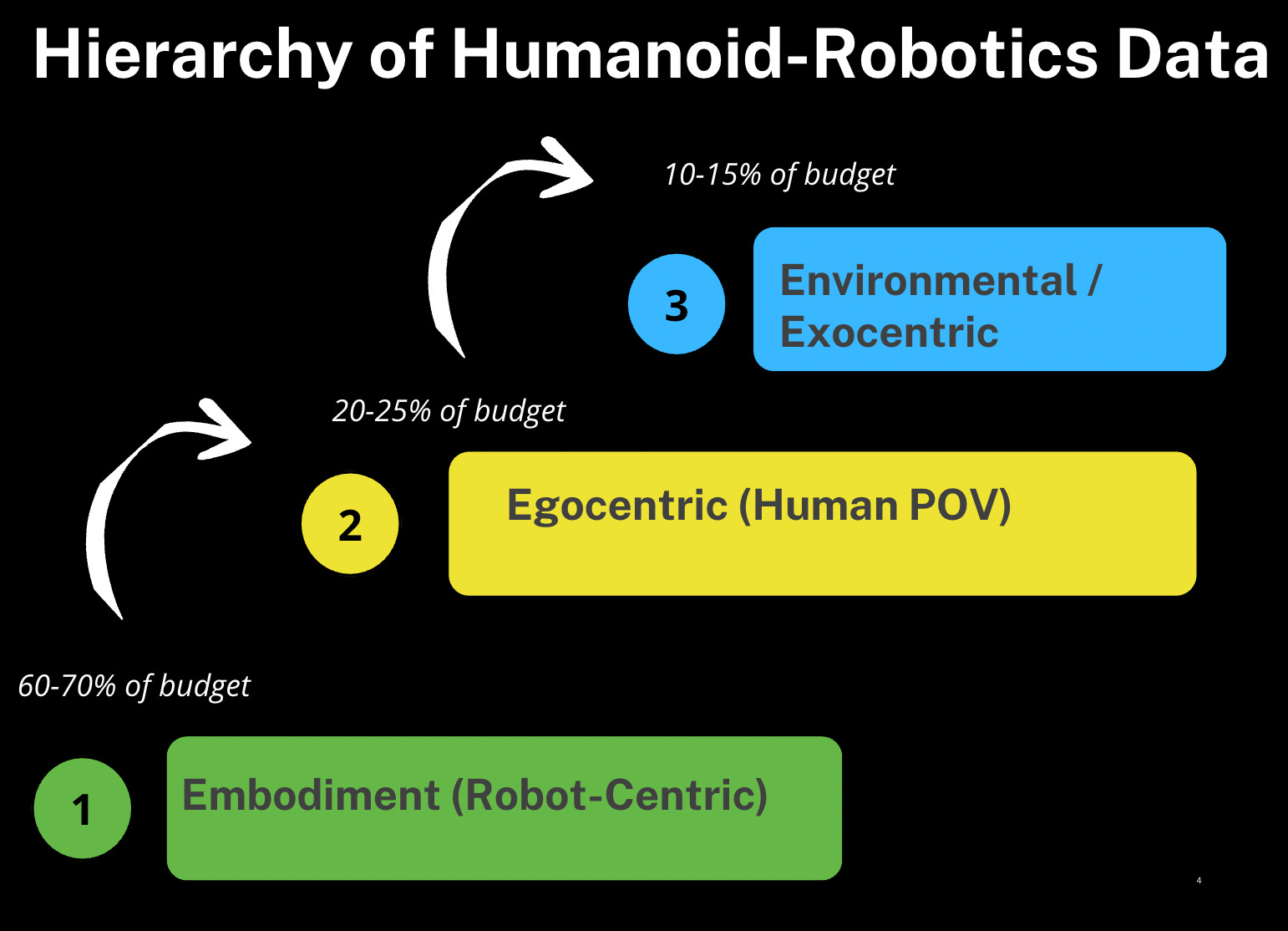

What is the hierarchy of data in humanoid robotics—embodiment, egocentric, and environmental—and how does each drive model performance?

Which dataset is in higher demand right now—egocentric human-POV video or embodiment tele-operation traces? And is egocentric simply easier to scale?

How do robotics companies choose between data infrastructure providers like Scale AI, iMerit, Sama, or Encord?

What a “typical volume contract” looks like for robotics/humanoid-data clients?

Who’s actually buying Scale AI’s Physical-AI data services today—and what do they keep in-house vs. outsource?

As humanoid platforms mature, do robotics OEMs keep using Scale AI as an external data partner, or does the role of third-party data providers shrink as companies internalize their own data engines?

How analogous are humanoid-robot data pipelines to those of autonomous vehicles?What lessons from AV data collection, labeling, and simulation transfer to Physical AI—and where do the workflows fundamentally diverge?

Please note: The insights presented in this article are derived from confidential consultations our team has conducted with clients across private equity, hedge funds, startups, and investment banks, facilitated through specialized expert networks. Due to our agreements with these networks, we cannot reveal specific names from these discussions. Therefore, we offer a summarized version of these insights, ensuring valuable content while upholding our confidentiality commitments.

Q1. Hierarchy of Data in Humanoid Robotics

Humanoid robotics is moving from polished demos to paid deployments, and the scarce input is no longer cameras or compute—it’s data that reliably turns perception into action on real hardware. For investors and systems integrators, the relevant asset isn’t a single “dataset,” but a hierarchy of training signals that compound: egocentric data to perceive and understand(why behind), environmental (exocentric) data to provide context and safety, and embodiment data to act and adapt on the target robot. This stack determines not only whether a robot can complete a task, but whether it can do so repeatably, safely, and at an economics that scales across sites.