Recent discussions have increasingly focused on SMCI, with clients raising deeper questions about whether to maintain positions or hedge against the stock. Clients are asking , “Legal talk would redefine the partnership between SMCI and NVIDIA?“, “$7B of finished goods and inventory—how much of that is truly transferable value versus written down?“ and many more. The current landscape suggests that the concerns surrounding the company have evolved from speculative claims into a more structured credibility challenge.

Source: US Senate

Last year in March 2025, NVIDIA CEO Huang told Bloomberg that there is no evidence of diversions when it comes to its Grace Blackwell chips. Furthermore, he added that Nvidia’s customers are well aware of the restrictions and that they are careful about it when selling to third parties.

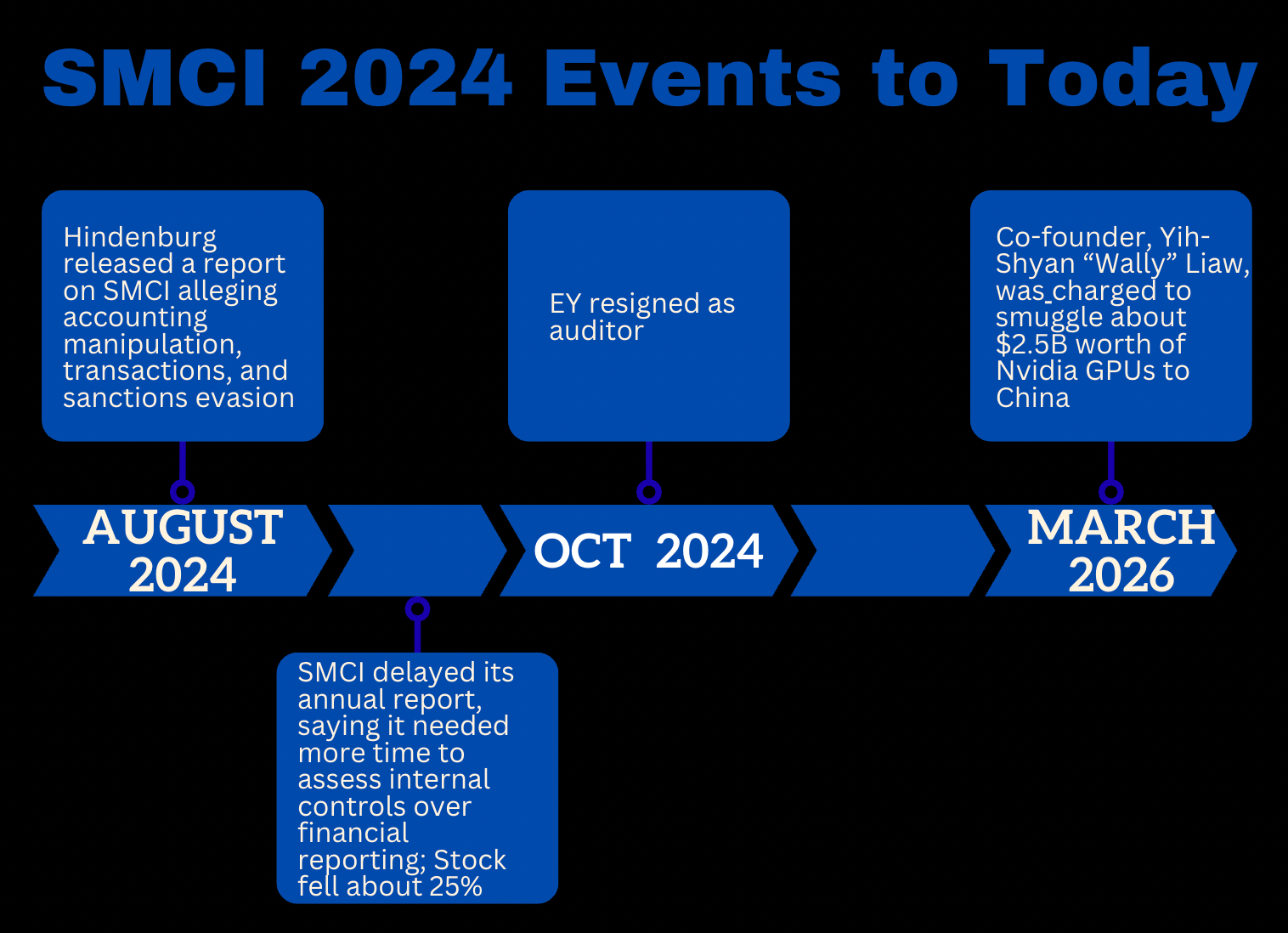

Now let’s rewind SMCI’s 2024 events to-date.

The shift in market sentiment for SMCI is defined by these key developments:

Initial 2024 Allegations: Hindenburg Research first brought forward a series of operational red flags.

Auditor Resignation: Ernst & Young (EY) subsequently stepped down, stating they could no longer rely on the company’s internal governance or the representations made by management.

2026 Legal Developments: A 2026 indictment has introduced criminal export-control allegations involving senior individuals linked to the firm.

While these legal filings do not necessarily validate every specific claim made by short-sellers, they appear to reinforce the market’s focus on governance and compliance. What might have been viewed as isolated noise in 2024 is now being re-evaluated as an early indicator of a more systemic internal control problem.

Investors also need to stop pretending the governance debate is separate from the commercial debate. EY resigned in 2024 saying it could no longer rely on management’s and the Audit Committee’s representations. SMCI’s special committee later said it found no substantial integrity concerns, said tone at the top was appropriate, and said EY’s conclusions were not supported by the facts it reviewed. But BDO later concluded SMCI did not maintain effective internal control over financial reporting as of June 30, 2025, citing multiple material weaknesses, including timely identification and disclosure of new related-party transactions. SMCI also disclosed that it received DOJ and SEC subpoenas in late 2024 following the August 2024 short-seller report.

That does not prove every historical allegation against the company. But it does mean the market is rational to apply a governance discount. And that matters because the key question in AI infrastructure is no longer just “Who can ship?” It is “Who can be trusted to ship, support, document, finance, and defend the shipment?”

For added context, this is not the first time internal-controls issues have been part of the SMCI story. In 2020, the SEC charged Super Micro and its former CFO over widespread accounting violations, and the company agreed to pay a $17.5 million penalty.

Ultimately, the progression from external accusations to an auditor’s exit and, finally, to a criminal indictment has shifted the narrative. The market is no longer just looking at a matter of public perception, but is now weighing whether these events point toward fundamental issues within the company’s leadership and regulatory adherence.

In today’s article, we’ll dig into the questions that have dominated recent client conversations:

Following the recent charges against senior-linked employees for illegal GPU exports, the question for every stakeholder is: does this indicate an isolated compliance failure, or a systemic governance issue that could redefine the partnership between SMCI and NVIDIA?

Is SMCI a real platform company with durable execution advantages, or was it just the fastest conduit for Nvidia demand?

If Nvidia never formally restricts SMCI but quietly shifts engineering priority, allocation timing, and support toward Dell, HPE, and ODMs, how quickly would that show up in win rates—and would the market recognize it before revenue breaks?

If large buyers of Blackwell or Rubin clusters are already rationally shifting 10–20% of future awards away from SMCI—either by splitting vendors or avoiding sole-source exposure—does that reveal that SMCI’s moat was never as deep as bulls believed, but instead dependent on speed, flexibility, and trust that can be re-underwritten elsewhere?

Inventory Is Not Just Big at SMCI — It Is Slower, More Finished, and More Exposed Than Bulls Admit: SMCI reportedly carries ~$7B of finished goods and inventory—how much of that is truly transferable value versus written down?

If SMCI were to enter a distressed or restructuring scenario, who are the natural acquirers of its assets—Dell, Hewlett Packard Enterprise, Lenovo, or ODMs like Quanta Computer / Wiwynn—and what would each actually want (customers, design wins, or inventory)?

Please note: The insights presented in this article are derived from confidential consultations our team has conducted with clients across private equity, hedge funds, startups, and investment banks, facilitated through specialized expert networks. Due to our agreements with these networks, we cannot reveal specific names from these discussions. Therefore, we offer a summarized version of these insights, ensuring valuable content while upholding our confidentiality commitments.